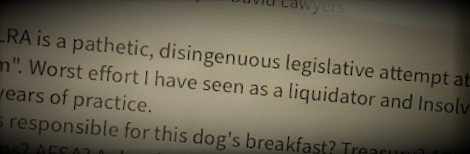

A pending new publication on corporate restructuring contains these comments about Code obligations of insolvency accountants advising financially distressed and

The concept of “potential” or “putative” insolvency administrators who have had “recent, long-term, substantial and remunerative involvement” with the company